Chapter 21 The role of pharmaceutical marketing

Introduction

This chapter puts pharmaceutical marketing into the context of the complete life-cycle of a medicine. It describes the old role of marketing and contrasts that with its continually evolving function in a rapidly changing environment and its involvement in the drug development process. It examines the move from the product-centric focus of the 20th century to the customer-centric focus of the 21st century.

Pharmaceutical marketing increased strongly in the 10–15 years following the Second World War, during which time thousands of new molecules entered the market ‘overwhelming’ physicians with new scientific facts to learn in order to safely and appropriately prescribe these breakthroughs to their patients. There was a great dependence on the pharmaceutical companies’ marketing departments and their professional sales representatives to give the full information necessary to support the prescribing decision.

Evidence-based marketing is based on data and research, with rigorous examination of all plans and follow-up to verify the success of programmes. Marketing is a general term used to describe all the various activities involved in transferring goods and services from producers to consumers. In addition to the functions commonly associated with it, such as advertising and sales promotion, marketing also encompasses product development, packaging, distribution channels, pricing and many other functions. It is intended to focus all of a company’s activities upon discovering and satisfying customer needs.

Management guru Peter F. Drucker claimed that marketing ‘is so basic it cannot be considered a separate function. … It is the whole business seen from the point of view of its final result, that is, from the customer’s point of view.’ Marketing is the source of many important new ideas in management thought and practice – such as flexible manufacturing systems, flat organizational structures and an increased emphasis on service – all of which are designed to make businesses more responsive to customer needs and preferences.

History of pharmaceutical marketing

There are not many accessible records of the types of marketing practised in the first known drugstore, which was opened by Arab pharmacists in Baghdad in 754, (http://en.wikipedia.org/wiki/Pharmaceutical_industry-cite_note-1) and the many more that were operating throughout the medieval Islamic world and eventually in medieval Europe. By the 19th century, many of the drug stores in Europe and North America had developed into larger pharmaceutical companies with large commercial functions. These companies produced a wide range of medicines and marketed them to doctors and pharmacists for use with their patients.

In the background, during the 19th century in the USA, there were the purveyors of tonics, salves and cure-alls, the travelling medicine shows. These salesmen specialized in selling sugared water or potions such as Hostetter’s Celebrated Stomach Bitters (with an alcoholic content of 44%, which undoubtedly contributed to its popularity). In the late 1800s, Joseph Myers, the first ‘snake oil’ marketer, from Pugnacity, Nebraska, visited some Indians harvesting their ‘medicine plant’, used as a tonic against venomous stings and bites. He took the plant, Echinacea purpurea, around the country and it turned out to be a powerful antidote to rattlesnake bites. However, most of this unregulated marketing was for ineffective and often dangerous ‘medicines’ (Figure 21.1).

Medical innovation accelerated in the 1950s and early 1960s with more than 4500 new medicines arriving on the market during the decade beginning in 1951. By 1961 around 70% of expenditure on drugs in the USA was on these newly arrived compounds. Pharmaceutical companies marketed the products vigorously and competitively. The tools of marketing used included advertising, mailings and visits to physicians by increasing numbers of professional sales representatives.

Back in 1954, Bill Frohlich, an advertising executive, and David Dubow, a visionary, set out to create a new kind of information company that could enable organizations to make informed, strategic decisions about the marketplace. They called their venture Intercontinental Marketing Services (IMS), and they introduced it at an opportune time, when pharmaceutical executives had few data to consult when in the throes of strategic or tactical planning. By 1957, IMS had published its first European syndicated research study, an audit of pharmaceutical sales within the West German market. Its utility and popularity prompted IMS to expand into new geographies – Great Britain, France, Italy, Spain and Japan among them. Subsequent acquisitions in South Africa, Australia and New Zealand strengthened the IMS position, and by 1969 IMS, with an annual revenue of $5 million, had established the gold standard in pharmaceutical market research in Europe and Asia. IMS remains the largest supplier of data on drug use to the pharmaceutical industry, providers, such as HMOs and health authorities, and payers, such as governments.

The medical associations were unable to keep the doctors adequately informed about the vast array of new drugs. It fell, by default, upon the pharmaceutical industry to fill the knowledge gap. This rush of innovative medicines and promotion activity was named the ‘therapeutic jungle’ by Goodman and Gilman in their famous textbook (Goodman and Gilman, 1960). Studies in the 1950s revealed that physicians consistently rated pharmaceutical sales representatives as the most important source in learning about new drugs. The much valued ‘detail men’ enjoyed lengthy, in-depth discussions with physicians. They were seen as a valuable resource to the prescriber. This continued throughout the following decades.

A large increase in the number of drugs available necessitated appropriate education of physicians. Again, the industry gladly assumed this responsibility. In the USA, objections about the nature and quality of medical information that was being communicated using marketing tools (Podolsky and Greene, 2008) caused controversy in medical journals and Congress. The Kefauver–Harris Drug Control Act of 1962 imposed controls on the pharmaceutical industry that required that drug companies disclose to doctors the side effects of their products, allowed their products to be sold as generic drugs after having held the patent on them for a certain period of time, and obliged them to prove on demand that their products were, in fact, effective and safe. Senator Kefauver also focused attention on the form and content of general pharmaceutical marketing and the postgraduate pharmaceutical education of the nation’s physicians. A call from the American Medical Association (AMA) and the likes of Kefauver led to the establishment of formal Continued Medical Education (CME) programmes, to ensure physicians were kept objectively apprised of new development in medicines. Although the thrust of the change was to provide medical education to physicians from the medical community, the newly respectable CME process also attracted the interest and funding of the pharmaceutical industry. Over time the majority of CME around the world has been provided by the industry (Ferrer, 1975).

The marketing of medicines continued to grow strongly throughout the 1970s and 1980s. Marketing techniques, perceived as ‘excessive’ and ‘extravagant’, came to the attention of the committee chaired by Senator Edward Kennedy in the early 1990s. This resulted in increased regulation of industry’s marketing practices, much of it self-regulation (see Todd and Johnson, 1992); http://www.efpia.org/Content/Default.asp?PageID=296flags).

The size of pharmaceutical sales forces increased dramatically during the 1990s, as major pharmaceutical companies, following the dictum that ‘more is better’, bombarded doctors’ surgeries with its representatives. Seen as a competitive necessity, sales forces were increased to match or top the therapeutic competitor, increasing frequency of visits to physicians and widening coverage to all potential customers. This was also a period of great success in the discovery of many new ‘blockbuster’ products that addressed many unmet clinical needs. In many countries representatives were given targets to call on eight to 10 doctors per day, detailing three to four products in the same visit. In an average call on the doctor of less than 10 minutes, much of the information was delivered by rote with little time for interaction and assessment of the point of view of the customer. By the 2000s there was one representative for every six doctors. The time available for representatives to see an individual doctor plummeted and many practices refused to see representatives at all. With shorter time to spend with doctors, the calls were seen as less valuable to the physician. Information gathered in a 2004 survey by Harris Interactive and IMS Health (Nickum and Kelly, 2005) indicated that fewer than 40% of responding physicians felt the pharmaceutical industry was trustworthy. Often, they were inclined to mistrust promotion in general. They granted reps less time and many closed their doors completely, turning to alternative forms of promotion, such as e-detailing, peer-to-peer interaction, and the Internet.

Something had to give. Fewer ‘blockbusters’ were hitting the market, regulation was tightening its grip and the downturn in the global economy was putting pressure on public expenditure to cut costs. The size of the drug industry’s US sales force had declined by 10% to about 92 000 in 2009, from a peak of 102 000 in 2005 (Fierce Pharma, 2009). This picture was mirrored around the world’s pharmaceutical markets. ZS Associates, a sales strategy consulting firm, predicted another drop in the USA – this time of 20% – to as low as 70 000 by 2015. It is of interest, therefore, that the USA pharmaceutical giant Merck ran a pilot programme in 2008 under which regions cut sales staff by up to one-quarter and continued to deliver results similar to those in other, uncut regions. A critical cornerstone of the marketing of pharmaceuticals, the professional representative, is now under threat, at least in its former guise.

Product life cycle

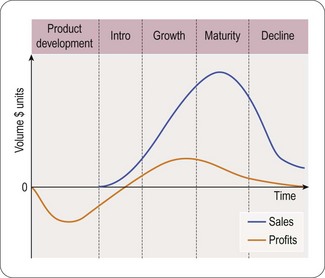

It is important to see the marketing process in the context of the complete product life cycle, from basic research to genericization at the end of the product patent. A typical product life cycle can be illustrated from discovery to decline as follows (William and McCarthy, 1997) (Figure 21.2).

The product’s life cycle period usually consists of five major steps or phases:

Product development phase

The product development phase begins when a company finds and develops a new product idea. This involves translating various pieces of information and incorporating them into a new product. A product undergoes several changes and developments during this stage. With pharmaceutical products, this depends on efficacy and safety. Pricing strategy must be developed at this stage in time for launch. In a number of markets for pharmaceuticals, price approval must be achieved from payers (usually government agencies). Marketing plans, based on market research and product strengths, for the launch and development of the product, are established and approved within the organization. Research on expectations of customers from new products should form a significant part of the marketing strategy. Knowledge, gained through market research, will also help to segment customers according to their potential for early adoption of a product. Production capacity is geared up to meet anticipated market demands.

Introduction phase

The introduction phase of a product includes the product launch phase, where the goal is to achieve maximum impact in the shortest possible time, to establish the product in the market. Marketing promotional spend is highest at this phase of the life cycle. Manufacturing and supply chains (distribution) must be firmly established during this phase. It is vital that the new product is available in all outlets (e.g. pharmacies) to meet the early demand.

Growth phase

The growth phase is the time the when the market accepts the new entry and when its market share grows. The maturity of the market determines the speed and potential for a new entry. A well-established market hosts competitors who will seek to undermine the new product and protect its own market share. If the new product is highly innovative relative to the market, or the market itself is relatively new, its growth will be more rapid.

Marketing becomes more targeted and reduces in volume when the product is well into its growth. Other aspects of the promotion and product offering will be released in stages during this period. A focus on the efficiency and profitability of the product comes in the latter stage of the growth period.

Maturity phase

The maturity phase comes when the market no longer grows, as the customers are satisfied with the choices available to them. At this point the market will stabilize, with little or no expansion. New product entries or product developments can result in displacement of market share towards the newcomer, at the expense of an incumbent product. This corresponds to the most profitable stage for a product if, with little more than maintenance marketing, it can achieve a profitable return. A product’s branding and positioning synonymous with the quality and reliability demanded by the customer will enable it to enjoy a longer maturity phase. The achievement of the image of ‘gold standard’ for a product is the goal. In pharmaceutical markets around the world, the length of the maturity phase is longer in some than in others, depending on the propensity of physicians to switch to new medicines. For example, French doctors are generally early adopters of new medicines, where British doctors are slow.

Decline phase

The decline phase usually comes with increased competition, reduced market share and loss of sales and profitability. Companies, realizing the cost involved in defending against a new product entry, will tend to reduce marketing to occasional reminders, rather than the full-out promotion required to match the challenge. With pharmaceutical products, this stage is generally realized at the end of the patent life of a medicine. Those companies with a strong R&D function will focus resources on the discovery and development of new products.

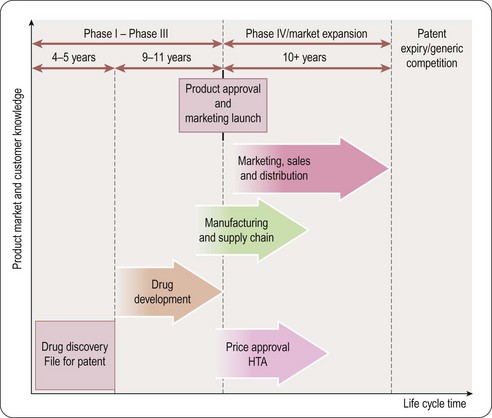

Pharmaceutical product life cycle (Figure 21.3)

As soon as a promising molecule is found, the company applies for patents (see Chapter 19). A patent gives the company intellectual property rights over the invention for around 20 years. This means that the company owns the idea and can legally stop other companies from profiting by copying it. Sales and profits will enable the manufacturer to reinvest in R&D:

• For a pharmaceutical product the majority of patent time could be over before the medicine even hits the market

• Once it is produced it takes some time for the medicine to build up sales and so achieve market share; in its early years the company needs to persuade doctors to prescribe and use the medicine

• Once the medicine has become established then it enters a period of maturity; this is the period when most profits are made

• Finally as the medicine loses patent protection, copies (generic products) enter the market at a lower cost; therefore, sales of the original medicine decline rapidly.

The duration and trend of product life cycles vary among different products and therapeutic classes. In an area of unmet clinical need, the entry of a new efficacious product can result in rapid uptake. Others, entering into a relatively mature market, will experience a slower uptake and more gradual growth later in the life cycle, especially if experience and further research results in newer indications for use (Grabowski et al., 2002).

Traditional Pharmaceutical marketing

Clinical studies

Pharmaceutical marketing depends on the results from clinical studies. These pre-marketing clinical trials are conducted in three phases before the product can be submitted to the medicines regulator for approval of its licence to be used to treat appropriate patients. The marketing planner or product manager will follow the development and results from these studies, interact with the R&D function and will develop plans accordingly. The three phases (described in detail in Chapter 17) are as follows.

Phase I trials are the first stage of testing in human subjects.

Phase II trials are performed on larger groups (20–300) and are designed to assess how well the drug works, as well as to continue Phase I safety assessments in a larger group of volunteers and patients.

Phase III studies are randomized controlled multicentre trials on large patient groups (300–3000 or more depending upon the disease/medical condition studied) and are aimed at being the definitive assessment of how effective the drug is, in comparison with current ‘gold standard’ treatment.

Marketing will be closely involved in the identification of the gold standard, through its own research. It is common practice that certain Phase III trials will continue while the regulatory submission is pending at the appropriate regulatory agency. This allows patients to continue to receive possibly life-saving drugs until the drug can be obtained by purchase. Other reasons for performing trials at this stage include attempts by the sponsor at ‘label expansion’ (to show the drug works for additional types of patients/diseases beyond the original use for which the drug would have been approved for marketing), to obtain additional safety data, or to support marketing claims for the drug.

Phase IV studies are done in a wider population after launch, to determine if a drug or treatment is safe over time, or to see if a treatment or medication can be used in other circumstances. Phase IV clinical trials are done after a drug has gone through Phases I, II and III, has been approved by the Regulator and is on the market.

Phase IV is one of the fastest-growing area of clinical research today, at an annual growth rate of 23%. A changing regulatory environment, growing concerns about the safety of new medicines, and various uses for large-scale, real-world data on marketed drugs’ safety and efficacy are primary drivers of the growth seen in the Phase IV research environment. Post-marketing research is an important element of commercialization that enables companies to expand existing markets, enter new markets, develop and deliver messaging that directly compares their products with the competition. Additionally, payer groups and regulators are both demanding more post-marketing data from drug companies.

Advantages of Phase IV research include the development of data in particular patient populations, enhanced relationship with customers and development of advocacy among healthcare providers and patients. These studies help to open new communication channels with healthcare providers and to create awareness among patients. Phase IV data can also be valuable in the preparation of a health economics and HTA file, to demonstrate cost effectiveness.

Identifying the market

At the stage when it appears that the drug is likely to be approved for marketing, the product manager performs market research to identify the characteristics of the market. The therapeutic areas into which the new product will enter are fully assessed, using data from standard sources to which the company subscribes, often IMS (Intercontinental Marketing Services). These data are generally historic and do not indicate what could happen nor do they contain much interpretation. The product manager must begin to construct a story to describe the market, its dynamics, key elements and potential. This is the time to generate extensive hypotheses regarding the market and its potential. Although these hypotheses can be tested, they are not extensively validated. Therefore the level of confidence in the data generated at this stage would not normally enable the marketer to generate a reliable plan for entry to the market, but will start to indicate what needs to be done to generate more qualitative and quantitative data.

When the product label is further developed and tested, further market research, using focus groups (a form of qualitative research in which a group of people are asked about their perceptions, opinions, beliefs and attitudes towards a new concept and the reasons for current behaviour) of physicians to examine their current prescribing practice and rationale for this behaviour. These data are extensively validated with more qualitative research. The identification of the target audiences for the new medicines is critical by this stage.

Traditionally, for the most part, the pharmaceutical industry has viewed each physician customer in terms of his/her current performance (market share for a given product) and potential market value. Each company uses basically the same data inputs and metrics, so tactical implementation across the industry is similar from company to company.

The product

Features, attributes, benefits, limitations (FABL)

A product manager is assigned a product before its launch and is expected to develop a marketing plan for the product that will include the development of information about the existing market and a full understanding of the product’s characteristics. This begins with Features, such as the specific mechanism of action, the molecular form, the tablet shape or colour. Closely aligned to this are the product Attributes, usually concrete things that reside in the product including how it functions. These are characteristics by which a product can be identified and differentiated. For example, these can include the speed of onset of action, absence of common side effects, such as drowsiness, or a once per day therapy rather than multiple doses. Then come the Benefits of the new product. Benefits are intrinsic to the customer and are usually abstract. A product attribute expressed in terms of what the doctor or patient gets from the product rather than its physical characteristics or features. A once per day therapy can lessen the intrusion of medicine taking on patient’s lives. Lack of drowsiness means the patient complies with the need to take the medicine for the duration of the illness and is able to function effectively during their working day. The benefits may also accrue to the physician as patient compliance indicates that the patient is feeling well, thanks to the actions of the doctor. It is critically important for the pharmaceutical marketer to maintain balance in promotional material. The Limitations of the product, where they could lead to the medicine being given to a patient for whose condition the medicine is not specifically indicated, must be clearly indicated in all materials and discussions with the doctor. The potential risk of adverse reactions of a medicine must also be clearly addressed in marketing interactions with medical professionals.

The analysis of the product in this way enables the marketer to produce a benefit ladder, beginning with the product features and attributes and moving to the various benefits from the point of view of the customer. Emotional benefits for the customer in terms of how they will feel by introducing the right patient to the right treatment are at the top of the ladder. It is also important for the product manager to construct a benefit ladder for competitive products in order to differentiate.

Armed with these data and the limited quantitative data, the product manager defines the market, identifies the target audience and their behaviour patterns in prescribing and assesses what must be done to effect a change of behaviour and the prescription of the new medicine once launched. A key classification of a target physician is his or her position in the Adoption Pattern of innovative new products. There are three broad classifications generally used:

• Early adopters/innovators: those who normally are quick to use a new product when it is available

• Majority: most fall into this category. There are the early majority and the late majority, defined by their relative speed of adoption. Some are already satisfied and have no need for a new product. Some wait for others to try first, preferring to wait until unforeseen problems arise and are resolved. Improved products (innovative therapies) may move this group to prescribe earlier

• Laggards/conservatives: this group is the slowest adopter, invariably waiting for others to gain the early experience. They wait for something compelling to occur, such as additional evidence to support the new product, or a new indication for which they do not currently have a suitable treatment.

Assessing the competition

It is critical for a product marketer to understand the competition and learn how to out-manoeuvre them. Market research is the starting point. A complete analysis of the competitive market through product sales, investment levels and resource allocation helps the marketer to develop the marketing plan for his own product. But it is important to understand the reason for these behaviours and critically evaluate their importance and success.

A comprehensive review of competitor’s activities and rationale for them is also necessary. Tools are available to facilitate this in the U.S., for example, PhRMA (the industry association), publish a New Medicines Database that tracks potential new medicines in various stages of development. The database includes medicines currently in clinical trials or at the FDA for evaluation (http://www.phrma.org/newmeds/). However, it is not just a desk bound exercise for a group of bright young marketers. Hypotheses, thus formed, must be tested against the customer perception of them.

The appearance of promotional aids, such as ‘detail aids’, printed glossies containing key messages, desktop branded reminder items (e.g. calendars), or ‘door openers’ (pens, stick-it pads, etc.) to get past the ‘dragon on the door’ (receptionist), are common, but do they work? In the pharmaceutical industry, for many years, marketing has been a little like the arms war. Rep numbers are doubled or tripled because that’s what the competition is doing. Identical looking detail pieces, clinical study papers wrapped in a shiny folder with the key promotional messages and product label printed on it, appear from all competitors. Regulations known as ‘medical-legal control’ are in place, internally and at a national level, to ensure that promotional messages are accurately stated, balanced and backed by well referenced evidence, such as clinical trial data and the approved product label.

Are promotional activities being focused on key leverage points and appropriate behavioural objectives? Before embracing what seems to be a good idea from the competition, the marketer needs to understand how this is perceived by the customer. New qualitative research needs to be conducted to gain this insight. One of the principal aims of successful marketing is to differentiate one product from another. It would, therefore, seem to be counter-intuitive for an assessment of competitor behaviour to conclude that copying the idea of a competitor is somehow going to automatically enable you to out-compete them. Much of traditional pharmaceutical marketing implementation has been outsourced to agencies. These organizations are briefed about the product, the market into which it will enter and the key therapeutic messages the company wishes to convey. The companies retain the preparation and maintenance of the marketing plan and, in general, leave the creative, behavioural side of the preparation to the agency. It is not, therefore, surprising that a formulaic approach to marketing delivery is the norm.

A classic example of this effect came in the 1990s with Direct to Consumer advertising (DTC). This form of direct marketing, in the printed media, television and radio, is legally permitted in only a few countries, such as the USA and New Zealand. Its original conception, for the first time, was to talk directly to patients about the sorts of medication that they should request from their physician. Anyone glued to breakfast television in the USA will be bombarded with attractive messages about what you could feel like if you took a particular medicine. These messages always contain a balance about contraindications and possible adverse reactions. Patients are encouraged to consult their physician. This concept was original and seems to have been effective in a number of cases (Kaiser Family Foundation, 2001) with increased sales volumes. Then practically every major company jumped on the bandwagon and competed for prime-time slots and the most attractive actors to play the role of patient. The appearance of these messages is practically identical and one washes over another. Probably the only people to pay them much attention, because of the volume and sameness, are the pharmaceutical marketers and the advertising agencies that are competing for the business. As for the physicians, little attention was paid to their reaction to this visual-media-informed patient.

In assessing how successful DTC has been, early data from the USA (Kaiser Family Foundation, 2001) observed, on average, a 10% increase in DTC advertising of drugs within a therapeutic drug class resulted in a 1% increase in sales of the drugs in that class. Applying this result to the 25 largest drug classes in 2000, the study found that every $1 the pharmaceutical industry spent on DTC advertising in that year yielded an additional $4.20 in drug sales. DTC advertising was responsible for 12% of the increase in prescription drugs sales, or an additional $2.6 billion, in 2000. DTC advertising did not appear to affect the relative market share of individual drugs within their drug class. In the decade to 2005 in the USA, spend on DTC practically tripled to around $4.2 billion (Donohue et al., 2007). This level of expenditure and impact on prescriptions has caused a great deal of controversy driven by traditional industry critics. However, some benefits have accrued, including the increased interaction between physicians and patients. In surveys, more than half of physicians agree that DTC educates patients about diseases and treatments. Many physicians, however, believe that DTC encourages patients to make unwarranted requests for medication.

From a marketing point of view, new concepts like DTC can prove helpful. Sales increase and patients become a new and legitimate customer. The cost of entry, particularly in financially difficult times can be prohibitive for all but a few key players. For those who are in this group, it becomes imperative that they stay there, as it is still a viable if costly segment. The naysayers are successfully containing DTC to the USA and New Zealand. The clarion calls for a moratorium and greater FDA regulation have still been avoided by those who market in this way. Will the investment in this type of marketing continue to pass the test of cost effectiveness and revenue opportunity? Competitive marketing demands a continuous critical assessment of all expenditure according to rigorous ROI (return on investment) criteria.

DTC advertising expenditure decreased by more than 20% from 2007 to 2009. Economic pressures and the global financial meltdown have resulted in a tighter budgetary situation for the pharmaceutical industry. These pressures have been strongly affected by rapidly disappearing blockbuster drugs and decreasing R&D productivity.

e-Marketing

e-Marketing is a process, using the internet and other electronic media, of marketing a brand or concept by directly connecting to the businesses of customers.

In pharmaceuticals, electronic marketing has been experimented with since the late 1990s. As a branch of DTC, it has been limited to only a couple of markets, the USA and New Zealand, because local laws elsewhere do not permit DTC communication about medicines. Some companies have created websites for physician-only access with some success, in terms of usage, but difficult to assess in terms of product uptake. Electronic detailing of physicians, that is use of digital technology: the Internet and video conferencing, has been used in some markets for a number of years. There are two types of e-detailing: interactive (virtual) and video. Some physicians find this type of interaction convenient, but the uptake has not been rapid or widespread, nor has its impact been accurately measured in terms of utility.

While e-Marketing has promise and theoretically great reach, the pharmaceutical industry in general has done little more than dabble in it. It is estimated to occupy around 1–3% of DTC budgets. Anecdotally staff recruited for their e-Marketing expertise have not integrated well into the highly regulated media market of the pharmaceutical industry.

CME

Continuing Medical Education is a long established means for medical professionals to maintain and update competence and learn about new and developing areas of their field, such as therapeutic advances. These activities may take place as live events, written publications, online programmes, audio, video, or other electronic media (see http://www.accme.org/dir_docs/doc_upload/9c795f02-c470-4ba3-a491-d288be965eff_uploaddocument.pdf). Content for these programmes is developed, reviewed, and delivered by a faculty who are experts in their individual clinical areas.

Funding of these programmes has been largely provided by the pharmaceutical industry, often through Medical Education and Communications Companies or MECCs. A number of large pharmaceutical companies have withdrawn from using these sorts of third-party agencies in the USA, due to the controversy concerning their objectivity. The Swedish health system puts a cap of 50% on the level of contribution to costs of the pharmaceutical industry.

This type of activity is beneficial to the medical community and provides, if only through networking, an opportunity to interact with the physicians. The regulation of content of these programmes is tight and generally well controlled, but a strong voice of discontent about the involvement of the industry continues to be sounded. The fact is that a key stakeholder in the medical decision-making process wants and benefits from these programmes, as long as they are balanced, approved and helpful. If the pharmaceutical industry wants to continue with the funding and involvement, then it should be seen as a legitimate part of the marketing template.

Key opinion leaders

Key opinion leaders (KOL), or ‘thought leaders’, are respected individuals in a particular therapeutic area, such as prominent medical school faculty, who influence physicians through their professional status. Pharmaceutical companies generally engage key opinion leaders early in the drug development process to provide advocacy and key marketing feedback. These individuals are identified by a number of means, reputation, citations, peer review and even social network analysis.

Pharmaceutical companies will work with KOLs from the early stage of drug development. The goal is to gain early input from these experts into the likely success and acceptability of these new compounds in the future market. Marketing personnel and the company’s medical function work closely on identifying the best KOLs for each stage of drug development. The KOL has a network which, it is hoped, will also get to know about a new product and its advantages early in the launch phase. The KOL can perform a number of roles, in scientific development, as a member of the product advisory board and an advisor on specific aspects of the product positioning.

The marketing manager is charged with maintaining and coordinating the company’s relationship with the KOL. Special care is taken by the company of the level of payment given to a KOL and all payments have to be declared to the medical association which regulates the individual, whatever the country of origin. KOLs can be divided into different categories. Global, national and local categorizations are applied, depending on their level of influence. Relationships between the company and a particular opinion leader can continue throughout the life cycle of a medicine, or product franchise, for example rheumatology, cardiovascular disease.

Pricing

Pharmaceutical pricing is one of the most complex elements of marketing strategy. There is no one answer as to how members of the industry determine their pricing strategy. Elements to consider are whether there is freedom of pricing at launch, such as in the USA, the UK and Germany, or regulated price setting as in France, Italy and Spain.

Freedom of pricing

The criteria for price setting are many and varied, including consideration of the market dynamics. Pricing of established therapies, the ability, or otherwise to change prices at a later stage than the product launch, the value added by the new product to the market and the perception of its affordability, are just some of the considerations. A vital concern of the company is the recovery of the costs of bringing the product to the market, estimated at an average of $1.3 billion for primary care medicines.

The marketing team, health economic analysts, financial function and global considerations are all part of the pricing plan. Cost-effectiveness analyses and calculations of benefit to the market are all factored into the equation. When a global strategy is proposed, market research is conducted along with pricing sensitivity analyses.

Regulated pricing

In the majority of markets where the government are also the payers, there is a formal process after the medical approval of a drug for negotiating a reimbursement price with the industry. The prices for multinational companies are set globally and the goal is to achieve the same or closely similar prices in all markets.

However, in matters of health and its perceived affordability each nation retains its sovereignty. Bodies such as the OECD gather and compare data from each of its 33 member states. The reports it issues highlight trends in pharmaceutical pricing and give each country easy access to the different approaches each regulator uses.

Different approaches abound throughout the regulated markets and include:

• Therapeutic reference pricing, where medicines to treat the same medical condition are placed in groups or ‘clusters’ with a single common reimbursed price. Underpinning this economic measure is an implicit assumption that the products included in the cluster have an equivalent effect on a typical patient with this disease

• Price-volume agreements, where discounts could be negotiated on volume commitments

• Pay for performance models, where rebates could be achieved if the efficacy is not as expected

• Capitation models where the expenditure is capped at a certain level.

There are a myriad of different approaches across the nations. The goal of these systems is generally cost containment at the government level. From a marketing point of view, the Global Brand Manager must be familiar with and sensitive to the variety of pricing variables. At the local level, a product manager needs to be aware of the concerns of the payer and plan discussions with key stakeholders in advance of product launch. Increasingly, the onus will be on the marketer to prove the value of the medicine to the market.

Prices with which a product goes to market rarely grow during the product life cycle in all but a few markets. However, there are frequent interventions to enforce price reductions, usually affecting the whole industry, in regulated markets over the marketed life of a medicine.

Health technology assessment (HTA)

Health technology assessment (HTA) is a multidisciplinary activity that systematically examines the safety, clinical efficacy and effectiveness, cost, cost-effectiveness, organizational implications, social consequences and legal and ethical considerations of the application of a health technology – usually a drug, medical device or clinical/surgical procedure (see http://www.medicine.ox.ac.uk/bandolier/painres/download/whatis/What_is_health_tech.pdf).

The development of HTAs over the 20 years prior to 2010 has been relatively strong. Before that, in the ’70s outcomes research assessed the effectiveness of various interventions. The Cochrane Collaboration is an international organization of 100 000 volunteers that aims to help people make well-informed decisions about health by preparing, maintaining and ensuring the accessibility of systematic reviews of the benefits and risks of healthcare interventions (http://www.cochrane.org/). INAHTA (International Network of Agencies for Health Technology Assessment) is a non-profit organization that was established in 1993 and has now grown to 50 member agencies from 26 countries including North and Latin America, Europe, Asia, Australia and New Zealand. All members are non-profit-making organizations producing HTAs and are linked to regional or national government. Three main forces have driven the recent developments of HTA: concerns about the adoption of unproven technologies, rising costs and an inexorable rise in consumer expectations. The HTA approach has been to encourage the provision of research information on the cost effectiveness of health technologies, including medicines.

NICE, the National Institute for Health and Clinical Excellence was established in the UK in 1999, primarily to help the NHS to eliminate inequality in the delivery of certain treatments, including the more modern and effective drugs, based upon where a patient lived. This became known as the ‘postcode lottery’. Over time, NICE also developed a strong reputation internationally for the development of clinical guidelines. In terms of the entry of new medicines and the assessment of existing treatments, NICE’s activities and influence attracted the attention of the global pharmaceutical industry. In the UK, NICE drew up and announced lists of medicines and other technologies it planned to evaluate. A number of health authorities used the impending reviews to caution practitioners to wait for the results of the evaluations before using the treatments. This became known, particularly in the pharmaceutical industry, as ‘NICE blight’. The phenomenon was magnified in importance by the length of time taken to conduct reviews and the time between announcement that a review was to take place and it taking place.

A NICE review includes the formation of a team of experts from around the country, each of whom contributes to the analysis. Data for these reviews are gathered from a number of sources including the involved pharmaceutical company. These reports involve a number of functions within a company, usually led by a health economics expert. The marketing and medical functions are also involved and, in a global company, head office personnel will join the team before the final submission, as the results could have a material impact on the successful uptake of a medicine throughout the world. The importance of the launch period of a medicine, the first 6 months, has been well documented by IMS (IMS, 2008b). Delays in the HTA review, having been announced, inevitably affect uptake in certain areas.

HTA bodies abound throughout the world. Their influence is growing and they are increasingly relied upon by governments and health services. The methodology used by these agencies is not consistent. Different governments use HTAs in different ways, including for politically motivated cost-containment ends. For the pharmaceutical company, the uncertainty caused by the addition of these assessments requires a new approach to the cost effectiveness and value calculations to ensure an expeditious entry into a market. New expertise has been incorporated into many organizations with the employment of health economists. Marketing managers and their teams have started to understand the importance of HTA in the life cycle of a new medicine. The added value and cost effectiveness of medicines are now a critical part of the marketing mix. It is clear that, in one form or another, HTAs are here to stay.

New product launch

The marketing plan is finalized and approved, the strategy and positioning are established, the price is set, the target audiences are finalized and segmented according to the key drivers in their decision-making process. It is now time to focus on the product launch.

Registration

When the medicine has been medically approved, there are formalities, different in each market concerning the registration and pricing approval.

Manufacturing and distribution

Product must be made for shipment, often through wholesalers, to retail outlets. Sufficient stock must be available to match the anticipated demand. Samples for distribution to physicians by reps will be made ready for launch.

Resource allocation

This is planned to ensure the product has the largest share of voice compared to the competition when launched. That is in terms of numbers and types of sales force (specialist and GP) according to the target audiences, and medical media coverage with advertising. In addition representative materials, including detail aids, leave behind brochures and samples.

Launch meeting

Sales representatives will have been trained in the therapeutic area, but the launch meeting will normally be their first sight of the approved product label. The positioning of the product and key messages will be revealed with the first promotional tools they will be given. The overall strategy will be revealed and training will take place. The training of reps includes practice in using promotional materials, such as detail aids, in order to communicate the key messages. Sometimes practising physicians are brought into the meeting to rehearse the first presentations (details) with the reps. Each rep must attain a high level of understanding, technical knowledge and balanced delivery before he or she is allowed to visit doctors.

Media launch

Marketing will work with public affairs to develop a media release campaign. What can be communicated is strictly limited in most markets by local regulation and limitations in direct to consumer (DTC) rules. It is a matter of public interest to know that a new medicine is available, even though the information given about the new medicine is rather limited.

Target audience

The launch preparations completed, it is time for the product to enter the market. The bright, enthusiastic sales force will go optimistically forward. In general, the maturity of the market and level of satisfaction with currently available therapy will determine the level of interest of the target audiences.

It is important to cover the highest potential doctors in the early stages with the most resource. The innovators and early adopters prescribe first and more than the others. The proportion varies by therapy area and by country, making around 5% and 10% of total prescriptions respectively. In a study from IMS covering launches from 2000 to 2005, an analysis of the effect of innovators, early adopters and early majority revealed these groups as being responsible for more than half of all prescriptions in the first 6 months from launch. After the first 6 months the late majority and conservative prescribers start to use the product. From this period on, the number of prescriptions begins to resemble that of the physicians in each of the groups (IMS, 2009).

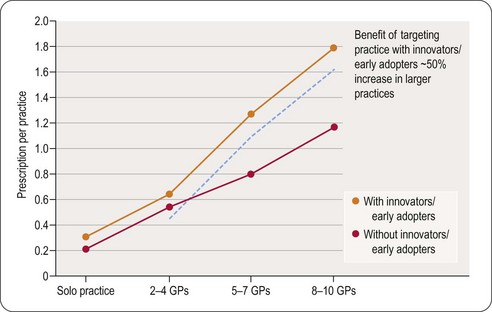

Another advantage of early focus on innovators is their influence on others in their group practice. In this case, prescribing per practice is higher than for equivalent-sized practices that lack an innovator prescriber (Figure 21.4).

The influence of innovators and early adopters on group prescribing

Patients driving launch success

Three types of patients make up the early uptake of medicines:

• New patients, who have not received previous drug therapy (e.g. Viagra; Gardasil)

• Switch patients, who have received another drug therapy

• Add-on patients, who have the new therapy added to their current treatment.

The success with which these types of patient are captured will determine the success of the launch and subsequent market share growth. An excellent launch tends to come as a result of the level of success in achieving switch patients. In most treatment areas there are a cohort of patients who are not responding well to existing therapy, or who suffer side effects from the treatment. The role of marketing in helping doctors to identify pools of existing patients is important, even before launch of the new product.

Early penetration of the market by targeting the right type of physicians and the right type of patients is predictive of continued success in the post-launch period, according to the IMS launch excellence study (IMS, 2009). A key predictor of success is the size of the dynamic market (new prescriptions, switches, plus any add on prescriptions) that a launch captures.

The first 6 months

IMS studies of launch excellence (IMS, 2008b; IMS, 2009) illustrate clearly that in a global product launch, the first 6 months are critical. Those that achieve launch excellence, according to the criteria above, continue to do well through the following stage of the life cycle. Those that do not achieve launch excellence rarely recover. Fewer than 20% of launches significantly improve their uptake trajectory between 6 and 18 months on the market after an unsuccessful early launch period.

Decline in prescriber decision-making power

A significant trend which represents a major challenge to traditional pharmaceutical marketing is the observed ongoing decline in the impact and predictability of the relationship between prescriber-focused promotional investment and launch market share achievement, in the early years of launch.

Implementing the market plan

Once the product has been successfully launched and is gaining market share, the role of marketing is to continue to implement the marketing plan, adjusting strategy as necessary to respond to the competitive challenge.

The process is of necessity dynamic. Results and changes in the market have to be continuously tracked and, as necessary, decisions should be re-evaluated. At the outset, the product manager develops a market map, according to the original market definition. Experience in the market will often necessitate the redrawing of parts of the map, according to the opportunity and barriers to entry.

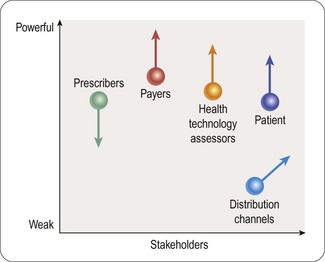

A customer portrait developed pre-launch will also need to be re-evaluated with experience in the market. The changing environment is identifying new customers and stakeholders, who are traditionally not engaged in the marketing process, including non-prescribers, e.g. payers and patients (Figure 21.5)

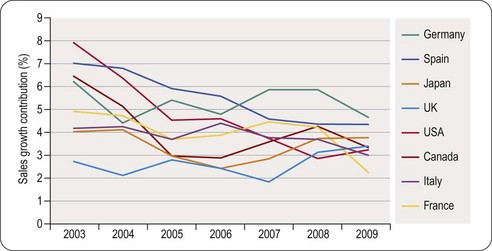

Life cycle management of the product is no longer an automatic process that gradually sorts itself out. It needs to be managed with the same enthusiasm and systematic rigor as a new product launch. The contribution to country growth from launches of products in the previous 3 years indicates a continued decline across the top eight pharmaceutical markets (Figure 21.6).

Changing environment – changing marketing

Traditional pharmaceutical marketing has served the pharmaceutical industry well over the past 60 years, but less so as we move on. The development of the market over time has the majority of the industry doing the same things and effectively cancelling each other out. The importance of differentiation from the competition is still high, whether the product or market is weak or strong. How can it be achieved? (See Box 21.1.)

Box 21.1

Competitive differentiation

| Product status/opportunities | |

| Weak or disappearing: | Strong or emerging: |

The philosophy of the 1990s and early 2000s was that ‘more is better’. More reps, more physician visits, more samples, more congresses and so on. All the while the old customer, the physician, was closing doors on sales reps, and losing trust in the industry’s motives and integrity. Additionally, the physician as provider is losing power as the principal source of therapeutic decision making. Within the traditional pharmaceutical marketplace, over 70% of marketing spend is focused on physicians. Does this allocation any longer make sense? Companies are structured and resourced in order to serve this stakeholder, not the other customers who are increasingly vital to the success or otherwise of new medicines.

The key stakeholder

Even more important, a new customer base is appearing, one of whose goals is to contain costs and reduce the rapid uptake of new medicines without any ‘perceived’ innovative benefit. At the time of introduction, this payer may be told of the ‘benefit’ claimed by the manufacturer. If the communicator of this message is an official of a health department, it is unlikely that they will be able, or motivated, to convince the payer of the claimed benefit. As the payers are rapidly taking over as the key stakeholder, it is imperative that the marketer talks directly to them. The pharmaceutical industry has viewed this stakeholder as something of a hindrance in the relationship between them and their ‘real’ customer, the doctor. It is likely that the feeling may be mutual. Industry has generally failed to understand the perspective and values of the payer, willing to accept an adversarial relationship during pricing and reimbursement discussions.

Values of the stakeholders

Decisions made on whether a new medicine adds value and is worth the investment depend on what the customer values. The value systems of the key stakeholders in the pharmaceutical medicine process need to be considered, to see where they converge or otherwise. A value system has been defined by PWC (2009) as ‘the series of activities an entity performs to create value for its customers and thus for the entity itself.’ The pharmaceutical value proposition ‘starts with the raising of capital to fund R&D, concluding with the marketing and resulting sale of the products. In essence, it is about making innovative medicines that command a premium price’.

The payer’s value system begins with raising revenue, through taxation or patient contribution. The value created for patients and other stakeholders is by managing administration and provision of healthcare. For the payer, the goal is to have a cost-effective health system and to enhance its reputation with its customers, or voters in the case of governments. It aims to minimize its costs and keep people well. At the time of writing, the UK health department is proposing a system of ‘value based pricing’ for pharmaceuticals, although no one seems to be able to define what it means.

The provider, in this case the physician, wants to provide high quality of care, economically and for as long as necessary. This stakeholder values an assessment of the health of a given population and to know what measures can be taken to manage and prevent illness.

The convergence of these three stakeholders’ value systems, says the PWC report, is as follows. ‘The value healthcare payers generate depends on the policies and practices of the providers used’; whereas providers generate value based on the revenues from payers and drugs that pharmaceutical companies provide. As for the pharmaceutical company the value it provides is dependent on access to the patients who depend on the payers and physicians. In this scenario each of the partners is by definition dependent on the others. An antagonistic relationship between these parties is, therefore, counterproductive and can result in each of the stakeholders failing to achieve their goals. A telling conclusion for the pharmaceutical industry is that they must work with payers and providers, to determine what sort of treatments the market wants to buy.

Innovation

Another conundrum for the pharmaceutical industry is the acceptance from the stakeholders of their definition of innovation. Where a patient, previously uncontrolled on one statin, for example, may be well controlled by a later entry from the same class, the payer may not accept this as innovative. They are unwilling to accept the fact that some patients may prefer the newer medicine if it means paying a premium to obtain it. With the aid of HTA (health technology assessment), the payer may use statistical data to ‘disprove’ the cost effectiveness of the new statin and block its reimbursement. The pharmaceutical company will find it difficult to recoup the cost of R&D associated with bringing the drug to the market. The PWC report (2009) addresses this problem by suggesting that the industry should start to talk to the key stakeholders, payers, providers and patients during Phase II of the development process. It is at this stage, they suggest, that pricing plans should start to be tested with stakeholders, rather than waiting until well into Phase III/launch. It is possible to do this, but the real test of whether a medicine is a real advance comes in the larger patient pool after launch. Post-marketing follow-up of patients and Phase IV research can help to give all stakeholders reassurance about the value added by a new medicine. It was in the 1990s, after the launch of simvastatin, that the 6-year-long 4S (Scandinavian Simvastatin Survival Study Group, 1994) study showed that treatment with this statin significantly reduced the risk of morbidity and mortality in at-risk groups, thus fundamentally changing an important aspect of medical practice. At Phase II, it would have been difficult to predict this. With today’s HTA intervention, it is difficult to see if the product would have been recommended at all for use in treatment.

R&D present and future

It has been said that the primary care managed ‘blockbuster’ has had its day. Undoubtedly R&D productivity is going through a slow period. Fewer breakthrough treatments are appearing (IMS, 2008a) as, in Germany ‘only seven truly innovative medicines were launched in 2007’, from 27 product launches.

More targeted treatment solutions are being sought for people with specific disease subtypes. This will require reinvention at every step of the R&D value chain. Therapies developed using advances in molecular sciences, genomics and proteomics could be the medicines of the future.

Big pharmaceutical companies are changing research focus to include biologicals and protein-based compounds (http://www.phrma.org/files/Biotech%202006.pdf). Partnerships between big pharma and biotech companies are forming to extend their reach and to use exciting technologies such as allosteric modulation to reach targets which have been elusive through traditional research routes. The possible demise of the traditional discovery approach may be exaggerated, but it highlights the need to rethink and revise R&D.

Products of the future

Generic versions of previous ‘blockbuster’ molecules, supported by strong clinical evidence, are appearing all the time, giving payers and providers choice without jeopardizing patient care. This is clearly the future of the majority of primary care treatment. But if a sensible dialogue and partnership is the goal for all stakeholders in the process, generics should not only provide care, but should also allow headroom for innovation.

It would seem reasonable that a shift in emphasis from primary to secondary care research will happen. It would also seem reasonable that the pharmaceutical industry will need to think beyond just drugs and start to consider complete care packages surrounding their medical discoveries, such as diagnostic tests and delivery and monitoring devices.

Marketers will need to learn new specialties and prepare for more complex interactions with different providers. Traditional sales forces will not be the model for this type of marketing. Specialist medicines are around 30% more expensive to bring to market. They treat smaller populations and will, therefore, demand high prices to recoup the development cost. The debate with payers, already somewhat stressed, will become much more important. The skills of a marketer and seller will of necessity stretch far beyond those needed for primary care medicines. The structure and scope of the marketing and sales functions will have to be tailored to the special characteristics of these therapies.

The future of marketing

If the industry and the key stakeholders are to work more effectively together, an appreciation of each other’s value systems and goals is imperative. The industry needs to win back the respect of its customers for its pivotal role in the global healthcare of the future.

The excess of over-enthusiastic marketing and sales personnel in the ‘more is better’ days of pharmaceutical promotion has been well documented and continues to grab the headlines. Regulation and sanctions have improved the situation significantly, but there is still lingering suspicion between the industry and its customers.

The most effective way to change this is greater transparency and earlier dialogue throughout the drug discovery and development process. Marketing personnel are a vital interface with the customer groups and it is important that they are developed further in the new technologies and value systems upon which the customer relies. Although they will not be the group who conduct the HTA reports from the company, they must be fully cognizant of the process and be able to discuss it in depth with customers.

Pharmaceutical marketing must advance beyond simplistic messages and valueless giveaways to have the aim of adding value in all interactions with customers. Mass marketing will give way to more focused interactions to communicate clearly the value of the medicines in specific patient groups.

The new way of marketing

Marketing must focus on the benefits of new medicines from the point of view of each of the customers. The past has been largely dominated by a focus on product attributes and an insistence on their intrinsic value. At one point, a breakthrough medicine almost sold itself. All that was necessary was a well-documented list of attributes and features. That is no longer the case.

It seems as if the provider physician is not going to be the most important decision maker in the process anymore. Specialist groups of key account managers should be developed to discuss the benefits and advantages of the new medicine with health authorities.

Payers should be involved much earlier in the research and development process, possibly even before research begins, to get the customer view of what medicines are needed from their point of view. Price and value added must be topics of conversation in an open and transparent manner, to ensure full understanding.

The future of marketing is in flux. As Peter Drucker said, ‘Marketing is the whole business seen from the customer’s point of view. Marketing and innovation produce results; all the rest are costs. Marketing is the distinguishing, unique function of the business.’ (Tales from the marketing wars, 2006). This is a great responsibility and an exciting opportunity for the pharmaceutical industry. It is in the interests of all stakeholders that it succeeds.

Donohue JM, Cevasco M, Rosenthal MB. A decade of direct-to-consumer advertising of prescription drugs. New England Journal of Medicine. 2007;357:673–681.

Ferrer JM. How are the costs of continuing medical education to be defrayed? Bulletins of the New York Academy of Medicine. 1975;51:785–788.

Fierce Pharma. Sales force cuts have only just begun – FiercePharma. Available online at http://www.fiercepharma.com/story/sales-force-cuts-have-only-just-begun/2009-01-20#ixzz15Rcr0Vn0, 2009.

Goodman LS, Gilman A. The pharmacological basis of therapeutics: a textbook of pharmacology, toxicology, and therapeutics for physicians and medical students, 2nd ed. New York: Macmillan; 1960.

Grabowski H, Vernon J, DiMasi J. Returns on research and development for 1990s new drug introductions, pharmacoeconomics, 2002. Adapted by IBM Consulting Services. Available online at http://www.aei.org/docLib/20040625_Helms.pdf, 2002.

IMS. Intelligence. 360: global pharmaceutical perspectives 2007, March 2008. Norwalk, Connecticut: IMS Health; 2008.

IMS. Launch excellence 2008, study of 3000 launches across 8 markets from 2000–7. Norwalk, Connecticut: IMS Health; 2008.

IMS. Achieving global launch excellence, January 2009. Norwalk, Connecticut: IMS Health; 2009.

Kaiser Family Foundation. Understanding the effects of direct-to-consumer prescription drug advertising, November 2001. Available online at www.kff.org/content/2001/3197/DTC%20Ad%20Survey.pdf, 2001.

Nickum C, Kelly T. Missing the mark(et). PharmExecutive.com, 2005. Sep 1, 2005

Pharmaceutical Research and Manufacturers of America (PhRMA). New Medicines Database and Medicines in Development: Biotechnology. http://www.phrma.org/newmeds/.

Podolsky SH, Greene JA. A historical perspective of pharmaceutical promotion and physician education. JAMA. 2008;300:831–833. doi:300/7/831 [pii]10.1001/jama.300.7.831

Price Waterhouse Cooper. Pharma 2020, which path will you take? Available online at http://www.pwc.com/gx/en/pharma-life-sciences/pharma-2020/pharma-2020-vision-path.jhtml, 2009.

Scandinavian Simvastatin Survival Study Group. Randomized trial of cholesterol lowering in 4444 patients with coronary heart disease: the Scandinavian Simvastatin Survival Study (4S). Lancet. 1994;344:1383–1389. PMID 7968073

Todd JS, Johnson KH. American Medical Association Council on Ethical and Judicial Affairs. Annotated guidelines on gifts to physicians from industry. Journal of Oklahoma State Medical Association. 1992;5:227–231.

Tales from the marketing wars: Peter Drucker on marketing. http://www.forbes.com/2006/06/30/jack-trout-on-marketing-cxjt0703drucker.html.

William D, McCarthy JE. Product life cycle: ‘essentials of marketing’. Richard D Irwin Company. 1997.